What Is Mat Tax Guru

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Minimum Alternate Tax Mat Section 115jb

Advance Tax Under Income Tax A Complete Guide

Strategic Analysis Of Amended Corporate Tax Rate Regime

Section 115baa And 115bab New Tax Rate For Companies

Itr 7 Indian Income Tax Return Taxguru

On minimum alternate tax mat alternate minimum tax amt a mat was introduced for the first time in the ay 1988 89.

What is mat tax guru. Applicability of mat mat is applicable to all companies including the foreign companies. Report from ca to be furnished electronically as per rule 12 2 in form 29b to certify book profits are computed as per sec 115jb. The effective tax rate for such companies will be 25 17 per cent inclusive of all surcharge and cess. 8 40 000 will amount to rs.

Current tax is the amount of income tax determined to be payable recoverable in respect of the taxable income tax loss for a period. Minimum alternative tax mat and its computation of book profit and mat credit under section 115jb of income tax act 1961. The minimum alternative tax mat is a provision introduced in direct tax laws to limit the tax deductions exemptions otherwise available to taxpayers so that they pay a minimum amount of tax to the government. Book profit of the company is rs.

Analysis of provision of section 115jb where in case of a company the income tax payable on the total income as computed under the income tax act in respect of any previous year is less than 15 of its book profit then such book profit shall be deemed to be the total income of the assessee and the tax. It is calculated on the basis of the book profits of a company not its. Tax 30 on rs. I normal tax liability or ii mat.

Report to be obtained in all cases irrespective of the fact that company pays mat or not since mat liability can be ascertained. Deferred tax is the tax effect of timing differences. Normal tax rate applicable to an indian company is 30 plus cess and surcharge as applicable. Such companies shall not be required to pay minimum alternate tax mat.

Mat is a tax provision reintroduced in 1997 in an attempt to bring zero tax high profits companies into the income tax net. Tax guru is a reliable source for latest income tax gst company law related information providing solution to ca cs cma advocate mba taxpayers. Minimum alternate tax mat rates for the a y. Timing differences are the differences between taxable income and accounting income for a period that originate in one period and are capable of reversal.

It was felt that due to various concession provided in tax laws big corporate groups become zero tax companies. Report of a accountant for mat.

Taxability Of Education Cess Issues Relating To Its Computation

Section 115jb Of Income Tax Act 1961 After Budget 2016

32 Income Tax Amendments Assessment Year 2020 21

Income Tax Rates For Financial Year 2019 20 And 2020 21

Tax Guru Taxation Laws Simplified Income Tax Act 1961 Ay 2020 21for B Com Bba

All About Deferred Tax And Its Entry In Books

Interest Payable U S 234a 234b 234c

Functionally Comparable Company Cannot Be Excluded From Comparables For Non Disclosure Of Rpt

Income Tax Incentives And Startup India Benefits Summary

Income Tax Amendments New Provisions Of Finance Act 2020

New Income Tax Regime Beneficial For You

Key Highlights Of Union Budget 2020 21 Finance Bill 2020

Penalties Under Income Tax Act 1961

Income Tax Rates For Financial Year 2020 21 Ay 2021 22

Direct Tax Compliance Calendar

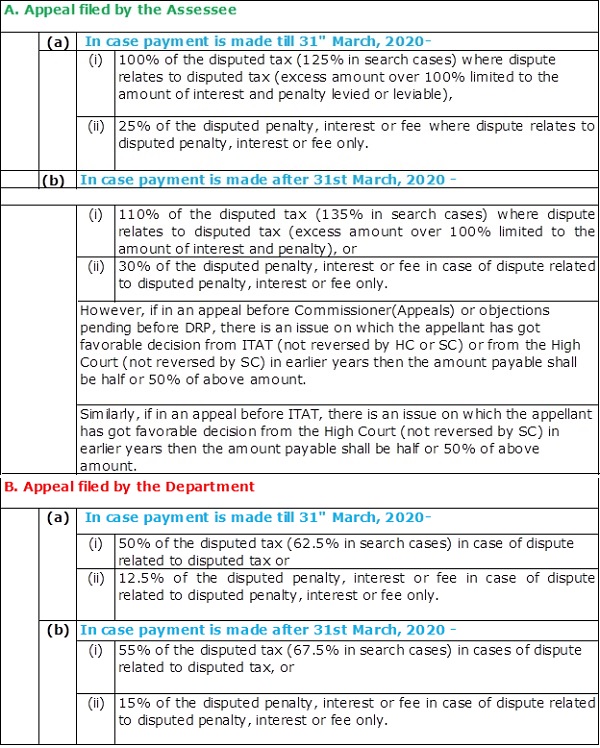

Direct Tax Vivad Se Vishwas Scheme 2020 Detailed Analysis

Set Off Of Bf Loss Mat Credit Adjustments Under New Tax Regime

Employee Share Based Payments And Its Taxation Aspects

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcrkvmluggbegfzohh3cvxqsbxqgtztelw T6refsnbvg6iqahc8 Usqp Cau

Income Tax Rate For Companies For Assessment Year 2020 21

Determination And Accounting Of Deferred Tax Asset And Liability

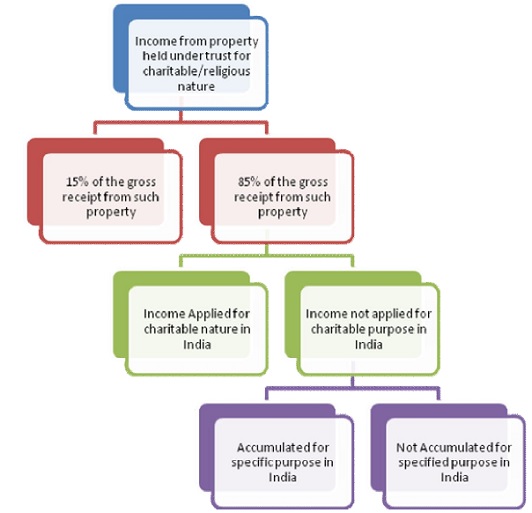

Taxation Of Charitable Religious Trust

Deduction Under Section 80ia 80ib Case Laws Assessment

Section 80 Iba Affordable Housing Scheme Income Tax Deduction

Income Tax Scrutiny Assessment And How To Avoid It

Section 270a 1 Penalty For Under Reporting Misreporting Of Income

Income Tax Amendments Applicable For Ay 20 21 Ay 21 22

Clarification On Passing Of Ordinary Special Resolution By Mca

Itat Upheld Addition For Accommodation Entry Receipts As Ltcg

S 40a 3 40a 2 Non Deduction Of Cash Expenses Payments To Relatives

Benefits Of Msme Registration Under Msme

Major Income Tax Form To Be Filed Along With Itr Due Date 30th September

Eatrzzmh4z Tm

Minimum Alternate Tax Mat U S 115jb Of Income Tax Act 1961 Taxact Income Tax Income

Taxation Of Partnership Firms And Llps

Summary Of Slab Deductions Under Income Tax Ay 2020 21

234abc Interest Calculator Brief With Examples

Summary Of Union Budget 2020 21

Goods And Service Tax Gst A Detailed Explanation With Examples

Income Tax Rates For Ay 2020 21 Fy 2019 20

Bogus Capital Gain No Adverse Inference Could Be Drawn Against Assessee On The Basis Of Untested Statements Without Allowing Opportunity Of Cross Examination

Do You Wanna Know How To Download Gst Certificate You Can Learn Making It Over Here On Taxguru Certificate Goods And Service Tax Registration